When it comes to the ongoing tension between fintech startups and banks, there’s no shortage of speculation regarding who will come out ahead. While it may seem like these two entities are perpetually at odds, the truth is there’s actually a substantial number of industry players on both sides of the fence that are cooperating with each other.

Loan applications’ exchanges, borrowers’ data exchanges between online transaction organisations and creditors, and collaborative studies on technological development are just a few examples where banks and fintech are collaborating. But the question still stands: How long can this uneasy truce last?

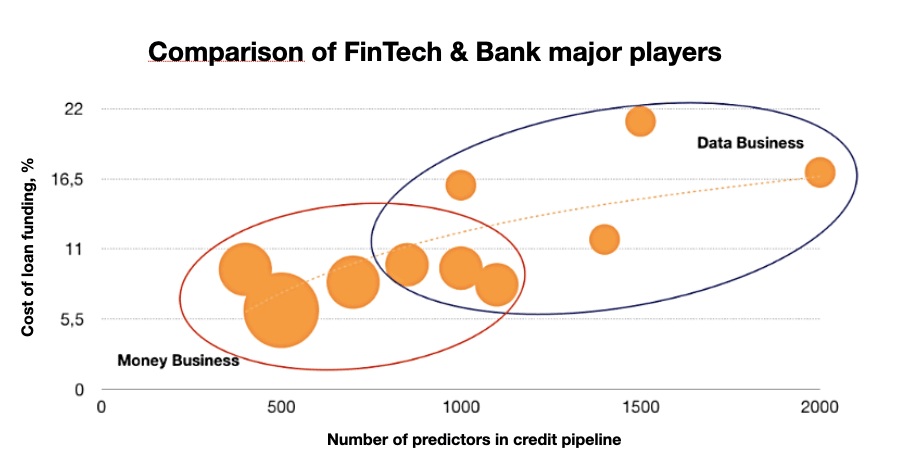

The JuicyScore team decided to take a deeper look into this phenomenon. We started with a detailed analysis of the major growth strategies in financial industry. As a result, we identified several fundamental factors influencing competitiveness in the industry. To simplify the overall picture, we focussed on the two major factors that define competitiveness in the retail assets business and that can be independently measured or estimated: 1) cost of funding, and 2) the amount of data used in credit conveyors.

Chart 1: Markers represent non-specific companies. The size of a marker indicates the proxy to amount of active clients who use credit products. Sources: The Central Bank of the Russian Federation, expert estimations

This chart shows that among the large number of growth strategies, the two most relevant are the reduction of the cost of funding (money business)and credit conveyor strengthening strategies (data business), which correspond in turn to the classic company sectors of Banking and FinTech.

The way various finance industry sectors will cooperate further depends on the extent of aspiration to compete in the nearby sectors, and on the way major features of the two key development trends within companies will develop in the future. To boil it down to layman’s terms: “You scratch my back, I’ll scratch yours.”

Let’s review these questions separately.

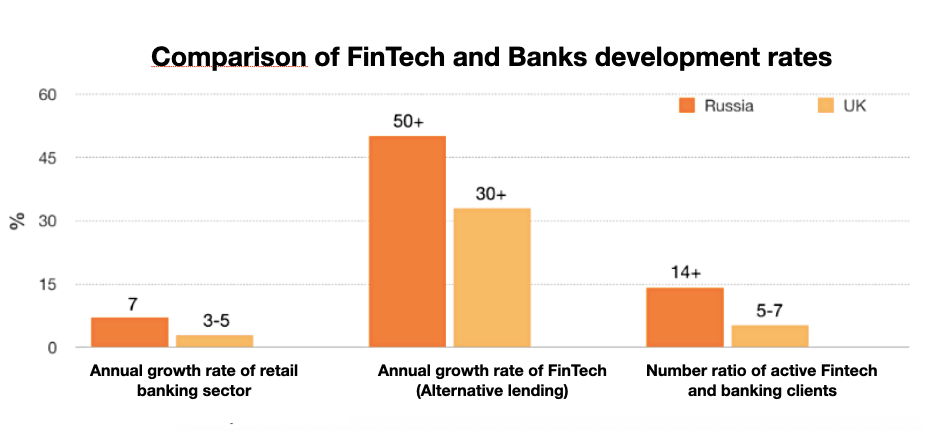

The aspiration to compete will be defined in many ways by the growth rates of these segments. Currently fintech sector growth is 5-10 times higher than the banking sector. Moreover, if we consider the clients’ base, the fintech sector volume is already at 10%+ of the total banking sector, and the gap between the sectors is rapidly narrowing. This trend is not unique to Russia (see Chart 2).

Chart 2: Fintech includes companies involved in alternative credit (alternative lending & online lending). Growth data for the industries for 2013-2017 have been estimated. Sources: Expert RA, the Central Bank of the Russian Federation, Bank of England

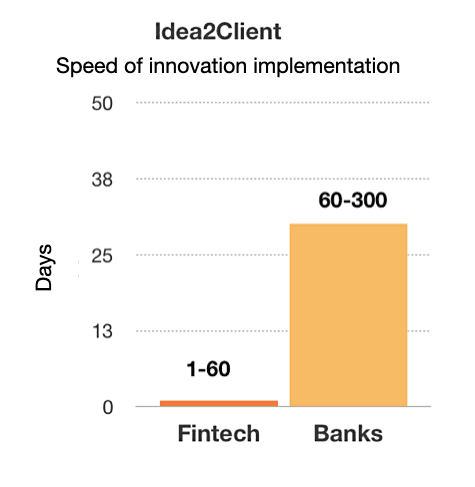

If we look in detail at the major competitive advantages of companies in the banking and fintech, two important aspects emerge—the pace of change/innovation implementation in products (Idea2Client time) and the rate that money is attracted (cost of funds).

Chart 3: Comparison of major growth drivers—Idea2Client and cost of credit funding

Despite the rapid introduction of agile approach in banks, fintech companies have significant advantages in implementation of the new ideas and innovations. These advantages are related not only to the widespread use of new technologies, but also to the working culture of fintech companies. We observed Agile-driven management in various forms in almost all fintech companies, and unlike banks, all key personnel with no exception (often including the CEO) worked on the product development and promotion; even including writing software code and taking part in product testing. Banks overcome that fintech superiority by attracting resources at significantly lower rates. This poses the question: How long will the banks retain their advantage? An analysis shows that the major fintech industry players can attract funds at rates comparable with average banks, and the gap is narrowing every year.

In the next few years, we will likely see the expansion of activities by leaders of the banking and fintech sectors. This expansion will also be due to the growth in related finance industry sectors. Most likely, we will witness a greater number of mergers and acquisitions in the market driven by desire of competing companies to gain a share of the market and/or to acquire a team of professionals and experts with the necessary competences.

Ultimately, there is one thing that will always bring the two sides together: the desire for growth.

Have a question for us about something that is relevant to the development of your business? Send your queries to info@juicyscore.com and we will do our best to cover them in our publications and studies.