We continue our series of articles about the meaningfulness of data describing the behavior of users on the Internet. In this article, we announce the launch of a global research project dedicated to studying users’ behavior, psychological types, and credit risks. The results of many recent studies have revealed that a person’s psychological type has a significant influence on his/her credit risk. There are a number of reasons:

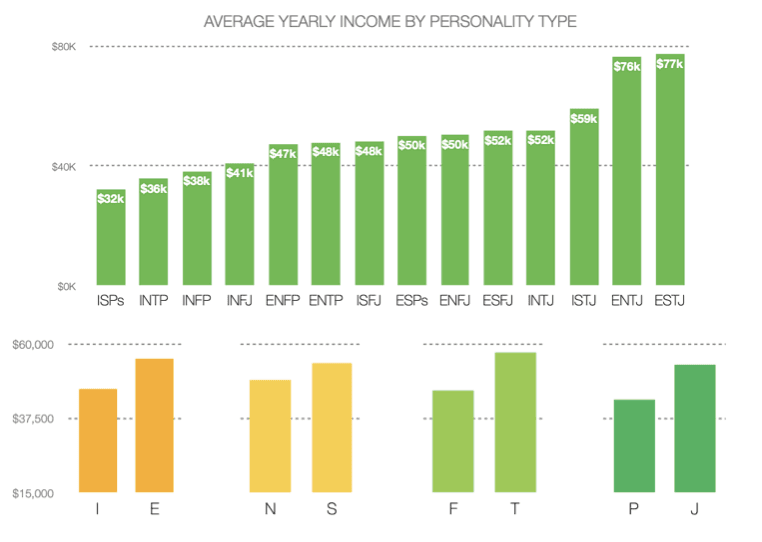

- First, our psychological type correlates with our income. If we take, for example, classification of psychological types, we will see that people with the psychological types characteristic of leaders (ESTJ/ENTJ) earn, on average, more than twice as much as the members of the ISFP/ISTP group, which is characteristic of people who work in the service sector or charity.

- Our psychological type is also strongly linked to how we spend. More expressive and sensitive people tend to buy more and take out consumer loans, and they use credit cards more frequently.

- Additionally, our psychological type determines how punctually we pay back loans and fulfill our promises and obligations. For example, people who are inclined to manage others and organize their work usually repay their loans more responsibly and try to avoid falling into arrears, even if money is tight.

The graph of average income with respect to a minimum level versus psychological type shows that there are significant differences in income among people with different psychological types.

* For more information research, please visit https://goo.gl/zwAJrc. The income of INTPs is taken as the basis (1).

Despite the fact that such connections do exist, the following problems have often arisen in connection with the use of this type of data:

- Difficulties associated with data collection. Until recent times, it was difficult to collect such data, since the average user spent 5–20 minutes filling out one questionnaire. Moreover, if completing a questionnaire was required in order to submit a loan application or place an order, the conversion rate decreased by 60–80%.

- The hit rate of non-intrusive data was low. For example, the social media hit rate was, on average, 60–85%, while clickstream data was plagued by low reliability because of the lack of sufficient historical information for a large user population.

According to our research, an analysis of the behavior and interests of people on the Internet can solve most of the problems associated with determining the psychological type of users. As an example, let’s discuss the differences between extraverts and introverts.

- An introvert: tries to read the information on the page; enters data at an even pace; rarely switches between tabs; sometimes uses ad blockers; has a relatively small number of active sessions on social networks; etc.

- An extravert: skims text; focuses on visual content or highlighted text; sometimes highlights certain text to focus on it; often switches between tabs; much less frequently uses ad blockers; has more active sessions on social networks and mail services; etc.

We plan to publish the full results of this research this autumn. Preliminary work has been done, but we plan to get a large amount of depersonalized data, which requires a great deal of time and significant investments in research.

If you are interested in our work, please contact us, and we will share the results with you.